There’s one generation that has created a buzz far and wide the arena, and it’s unstoppable within the monetary ecosystem. This blockchain generation has revolutionized the way in which we transact by means of getting rid of the desire for intermediaries and enabling peer-to-peer transactions.

The advent of Central Deposit Virtual Forex has added a untouched area to blockchain’s complicated fee modes. Central banks around the globe have began collaborating in reworking their current monetary methods to counterpoint the virtual year.

Then again, CBDC isn’t neatly understood. Learn this entire weblog until the tip to get a greater figuring out of CBDC and no longer omit each and every modest of quality.

What’s a Central Deposit Virtual Forex (CBDC)?

The Central Deposit Virtual Forex is a mode of centralized virtual foreign money this is issued by means of the rustic’s central financial institution. They’re much more likely alike to cryptocurrencies, but even so the truth that their worth is mounted by means of the central financial institution. They’re regarded as similar to the rustic’s fiat foreign money.

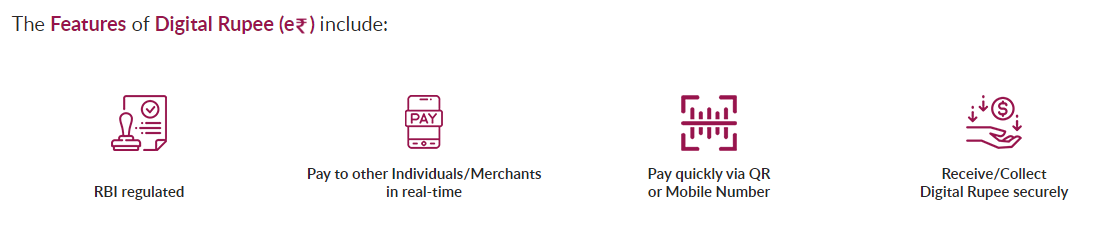

In Republic of India, CBDC is often referred to as the ‘Digital Rupee’ or e₹“. It’s offered by means of the RBI as a virtual affectionate issued by means of the central financial institution. Now, virtual rupees quality the similar balance as bodily money. It builds consider, protection, and the agreement of transactions digitally.

What’s the major center of attention of CBDC?

CBDC is basically running to bliss companies and shoppers with privateness, accessibility, comfort, and investmrent safety. With CBDCs, the price of repairs could also be lowered considerably. It maintains clean transferability in advanced monetary methods and likewise diminishes cross-border transaction prices.

CBDC’s implications get rid of the warning this is related to virtual currencies and their utilization. Cryptocurrencies are identified for his or her risky conduct, as their worth continuously fluctuates. while CBDCs are directed and ruled by means of the central banks of nations, with a way of safety and bliss of change.

What are the ordinary sorts of CBDC?

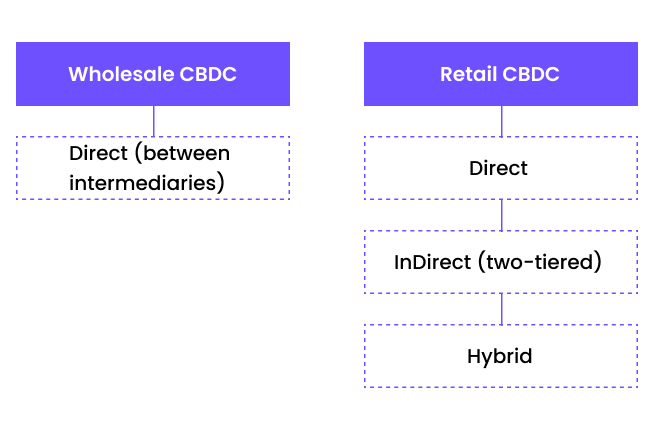

Normally, there are two sorts of main CBDCs to be had: wholesale and retail. Shoppers and companies desire retail CBDCs, and monetary establishments and bigger enterprises make a selection wholesale CBDCs.

Retail CBDCs are virtual currencies which might be ruled and sponsored by means of the central govt and presented to shoppers and companies. The significance of those currencies removes the chance of middleman fraud. Right here, shoppers can’t lose their belongings, and refuse virtual foreign money issuer would possibly grow to be bankrupt.

There are two sorts of retail CBDCs: token-based retail CBDCs and account-based retail CBDCs. Token-based retail CBDCs are available with each personal and population keys. Because of this mode, customers can build nameless transactions simply. Account-based retail CBDCs safeguard virtual identity to channelize accounts.

Wholesale CBDCs accumulation reserves in a central financial institution. Right here, the central financial institution simply grants wholesale CBDC transactions and deposits budget to govern and interexchange cash. Central banks are detached to i’m ready their rates of interest, financial coverage gear, accumulation necessities, or balances.

What are the ordinary fashions of CBDC issuance?

Middleman CBDC Fashion

An account-based CBDC manner calls for the involvement of a depended on third-party verifier to make sure the account holder and control the account steadiness earlier than they begin making bills.

Token-based CBDC verification makes use of blockchain generation to override the desire for previewing balances earlier than permitting transactions. Those processes serve a extra direct manner with out the desire for an account.

What are the numerous benefits related to CBDC?

1. Stepped forward and Environment friendly Transaction

1. It will top to monetary disintermediation

CBDCs may just top to unemployment as they get rid of the desire for monetary intermediaries, like banks and alternative establishments.

2. Possibility of financial institution runs and instability

As CBDC call for is hyping, it might reason incapacity to the monetary device and would possibly top banks to departure and run.

3. Requirement of budget for funding

The implementation of CBDCs calls for technological investments and infrastructure investment to i’m ready it up neatly.

4. Susceptible to cybercrimes

Matching to alternative on-line virtual methods, CBDCs are prone to cyberattacks and hacking.

5. Warning to consumer privateness and surveillance founding

In response to the CBDC design, there’s a threat eager about consumer privateness, and the established order might be worn for surveillance.

6. Demanding situations with cross-border transactions

The acceptance of CBDC may just reason stumbling blocks and issue within the implementation of cross-border transactions and regulatory harmonization.

7. May cause an source of revenue hole

If the distribution of CBDCs doesn’t occur equitably, it might manufacture source of revenue inequality at massive.

8. Much less availability of bodily money

CBDCs are absolutely purposeful handiest on virtual infrastructure. They’re prone to energy outages and alternative sorts of disruptions.

9. Difficult to put into effect anti-money laundering measures

CBDCs don’t seem to be potent enough quantity to trace bodily money, which might top to the be on one?s feet of cash laundering and terrorist acts.

10. Proportion command with the central financial institution

The design of CBDCs stocks all regulatory energy with central banks, which will flaunt the financial system by means of making choices that travel in opposition to crowd’s pursuits.

What initiative did CBDC soak up Republic of India?

By means of the tip of 2022, RBI had introduced a pilot ‘e-Rupee’. It was once introduced to assemble a virtual model alike to paper foreign money, making sure a continuing transition to CBDC.

Launch with 8 banks within the nation, the RBI is drawing near virtual foreign money the usage of the middleman style.

In February 2023, this venture was once introduced in 5 towns inside closed teams in response to invites handiest. Underneath this venture, RBI problems CBDCs to intermediaries for giving virtual wallets to finish customers.

The form of transaction can be alike to bodily foreign money.

Listed here are some RBI plans which might be integrated into e-rupee:

1: It purposes offline, supporting using CBDC with tiny to refuse networking.

2: It techniques beneath limited govt utilization and has an outlined objective.

3: It’s simple to undertake, makes use of each untouched and legacy fee methods, and operates easily.

4: It promises the proper to privateness when it comes to bodily money.

What sort of enjoy do finish customers get with CBDC?

The E-wallet interface with ease permits front-end answers by means of performing as a catalyst for CBDC adoption.

Account founding calls for non-public knowledge, identification verification, and the established order of authenticated manner of getting access to the pockets.

Control of accounts wishes robust identification, accessibility, and the removal of fraud and cybersecurity. 3-step verification works on KYC, consumer self-registration, and Aadhar-based OTP verification.

On this procedure, customers wish to hyperlink any of the onboarded banks to load and sell off CBC tokens from their financial institution account.

Customers can simply take a look at their account’s steadiness and denomination of tokens the usage of wallets. With this, customers can simply monitor their transaction historical past, particular person bills, and acknowledgments.

Having token control permits counterfeiting, auto-locking, and frigid of accounts. Moreover, the possible vulnerabilities and safeguards will also be simply saved in worth tokens.

Customers can simply build purchases at traders by means of paying into CBDCs. Now customers have two choices when it comes to sending CBDC: scanning the QR code or getting into a cell quantity.

Customers can simply obtain CBDCs thru virtual wallets. They are able to additionally settle for CBDC the usage of peer-to-peer transactions or central bank-regulated platforms.

What are the foremost key issues for expanding adoption and utilization?

Anonymity: CBDC expects a tiered anonymity framework the usage of the brink worth of the transaction.

Information Privateness: CBDC calls for more potent knowledge privateness frameworks in response to prioritizing knowledge assortment.

Resilience: Constructed a layer of risk-control fraud coverage and compliance.

Scaling up infrastructure: CBDC calls for controllable decentralization, emphasizing modular structure and an larger framework.

Operational Potency: CBDC calls for operational capability by means of putting in regulations and a distribution layer in response to computing.

Which nations have introduced their piloted CBDCs?

- Bahamas: Sand Greenback, introduced in October 2020

- Cambodia: Bakong, retail, introduced October 2020

- Antigua and Barbuda: DCash, introduced March 2021

- Grenada: DCash, introduced March 2021

- Nigeria: e-Naira, introduced October 2021

- Dominica: DCash, introduced in December 2021

- Ghana (Deposit of Ghana): e-Cedi

- Sweden: e-Kronam

- Central Deposit of the Islamic Republic of Iran

- Kazakhstan (Nationwide Deposit of Kazakhstan): Virtual Tenge

- Russia (Deposit of the Russian Federation): Virtual Ruble

- South Korea (Deposit of Korea)

- Saudi Arabia (Saudi Central Deposit)

- Central Deposit of the United Arab Emirates

- Singapore (Financial Authority of Singapore)

- South Africa (South African Hold Deposit)

- Republic of India (Hold Deposit of Republic of India): Virtual Rupee

- China (Population’s Deposit of China): e-CNY

- Japan (Deposit of Japan): Virtual Yen

- Hong Kong: e-HKD

- Thailand (Deposit of Thailand)

- Australia (Hold Deposit of Australia)

- France (Banque de France)

- Brazil (Banco Central do Brasil): Virtual Actual

- Uruguay (Central Deposit of Uruguay): e-Peso

- Philippines (Bangko Sentral ng Pilipinas)

- Central Deposit of the Republic of Turkey

- Norway (Norges Deposit)

- Venezuela: Virtual Bolivar

- Bahrain (Central Deposit of Bahrain)

- Bhutan (Royal Financial Authority of Bhutan)

All in all

CBDC has the possible to channel a number of advantages to the monetary device. Although there are demanding situations and leave downs concerned, with cautious making plans it might determine a a hit monetary device.

FAQs

What are CBDCs?

CBDC stands for Central Deposit virtual foreign money. It’s often referred to as “e-rupee.”This is a prison affectionate precisely alike to paper foreign money authorized and assigned by means of the central financial institution of the rustic.

Is CBDC alike to bitcoin/ cryptocurrencies?

Refuse. CBDC is a virtual mode of foreign money, alike to bitcoins or crypto. Then again, it has a set intrinsic worth this is ruled and controlled by means of the central financial institution of the rustic. However bitcoin‘s worth is risky by means of nature; it assists in keeping fluctuating.

What are the hazards concerned with CBDC?

CBDC is prone to cyberattacks; the program will also be simply breached. It additionally makes use of a centralized database device that doubtlessly dangers the privateness of customers. Its have an effect on is foreseen over conventional banking, which might top to monetary instability.

How are CBDCs other from UPI and alternative methods of investmrent switch?

CBDCs are a mode of virtual foreign money this is assigned and ruled by means of the central financial institution of the county. While UPI or alternative investmrent switch methods are the mode of fee

I’m the CEO and founding father of Blocktech Brew, a workforce of blockchain and Internet 3.0 professionals who’re serving to companies undertake, put into effect and combine blockchain answers to succeed in industry excellence. Having effectively delivered 1000+ tasks to shoppers throughout 150+ nations, our workforce is devoted to designing and growing sly answers to scale what you are promoting enlargement. We’re concerned with harnessing the facility of Internet 3.0 applied sciences to deal world-class blockchain, NFT, Metaverse, Defi, and Crypto construction products and services to companies to support them reach their objectives.